B2B marketplaces are experiencing explosive growth and so are the recipes for their success. Received wisdom is that the more payment options an online marketplace offers à la Amazon, the better. But is this really the case, and does it apply equally to B2B marketplaces? In this post we’ll explore the pros and cons and how to choose the right buyer payment options for your nascent B2B marketplace. Let’s dive in.

Advantages of Multiple B2B Payment Methods

Offering a variety of payment methods isn’t just about convenience – it’s a strategic move that can significantly boost your marketplace’s success.

Flexibility for Buyers

Offering a variety of payment methods allows buyers to choose what suits them best. Some may prefer credit cards, while others might opt for wire transfers or digital payment platforms. By accommodating different preferences, you enhance the overall user experience and improve conversion rates.

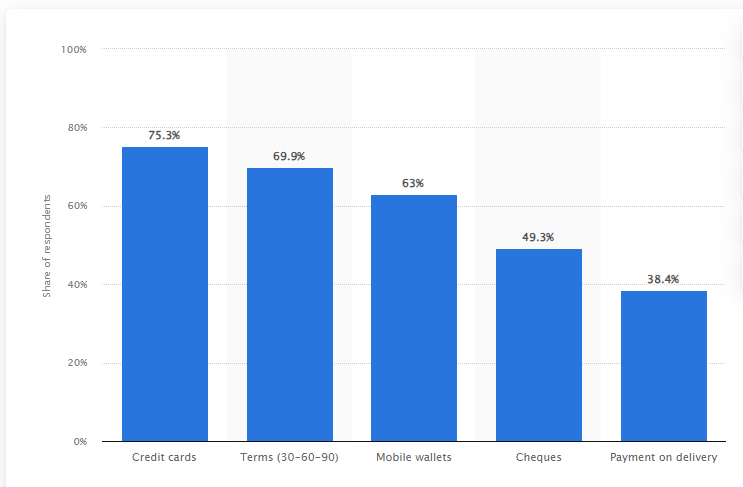

A 2020 Statista survey showed that most companies offered payment through credit cards for B2B purchases, while 63% integrated mobile wallets in their e-commerce.

Global Reach

B2B marketplaces often serve international audiences. Supporting multiple currencies and payment methods ensures that buyers from various regions can transact seamlessly. For example, Stripe Connect enables the onboarding of vendors from 35+ countries without the need to establish local entities.

Risk Mitigation

Diversifying payment options reduces risk. If one method encounters issues (e.g. technical glitches or regulatory changes), alternative options remain available.

Competitive Edge

A marketplace that offers convenient payment choices stands out among competitors. Buyers are more likely to choose platforms that align with their preferred methods.

Deciding on Currencies & Payment Methods

So, how do you curate the perfect payment buffet? Consider the following ‘ingredients’:

- Target audience: Research your buyers’ preferred payment methods based on industry, region, and transaction size. For instance, credit cards dominate smaller purchases, while bank transfers (ACH, SWIFT, EFT) reign supreme for high-value deals.

- Local considerations: Offer options aligned with regional preferences and regulations. Think Alipay for China or SEPA for the Eurozone. MobyPark, a parking marketplace, expanded its European footprint by offering the IDEAL payment option to its Dutch customers.

- Cost-effectiveness: Weigh processing fees against transaction volume and the value each method brings. Remember, high-cost options like Amex might only be suitable for premium offerings.

- Don’t forget about the technical aspect. Some payment methods might be easier to integrate than others. Stripe Connect, for example, offers an extensive bouquet of payment methods geared towards marketplace platforms. Its implementation, though, requires careful alignment with your marketplace business model.

Finding “Payment-Method Fit”

Remember, payment options aren’t static. Stay agile and experiment! A/B test different options to see what resonates with buyers. Platforms like Mirakl, a SaaS marketplace solution, takes payment options to a granular level to boost Payment-Method Fit. Mirakl allows sellers to define their preferred payment methods, giving buyers flexibility while respecting seller preferences.

Expanding B2B Payment Options to improve Product-Market Fit

83% of B2B buyers see a smooth payment and checkout experience as a top priority when choosing a B2B supplier platform.

Survey by Balance, a B2B ecommerce payments platform

Testing and expanding payment options can play a crucial role in enhancing the product-market fit for B2B marketplaces. Grainger, a marketplace for industrial supplies, saw a 17% increase in average order value after introducing a virtual credit card solution for their B2B customers.

It’s not just about offering a vast array of choices though. Introduce new payment options, track their usage, and analyse the impact on conversions. Relevant data helps you refine your offerings and ensure they align with user needs. For example, some B2B transactions involve large sums, so offering options like ACH transfers or net terms (payment after a specific period) might be essential.

FashionGo, a wholesale marketplace for fashion items, introduced an AI-enhanced financing service that offers Dynamic Net Terms to small and medium business buyers. This hybrid payment option offers buyers a personalised mix of immediate and deferred terms based on their credit rating, order history and business needs.

Payment options should benefit both buyers and sellers. This often leads to the conundrum of buyers who would like the longest payment terms possible, while sellers have to protect their clash flow. A Buy Now, Pay Later (BNPL) option can solve this by offering buyers instalments, while paying sellers up front.

Challenges in Implementing Multiple B2B Payment Methods

While offering multiple payment methods in B2B marketplaces improves product-market fit, it also presents several challenges:

Technical Integration

- Complexity: Integrating each payment gateway requires coding and configuration, increasing development time and resource needs.

- Compatibility: Maintaining compatibility between the marketplace platform and various payment gateways can be complex, requiring ongoing maintenance and updates.

- Security: Each integration introduces a new potential security vulnerability, requiring robust security measures to prevent breaches and unauthorised access.

Managing Transaction Fees

- Variable Costs: Each payment method often comes with its own transaction fee structure, introducing complexity in calculating and managing these fees for both buyers and sellers.

- Price Transparency: Clearly communicating the associated fees for each payment method to both buyers and sellers is crucial to avoid confusion and potential disputes.

- Marketplace Revenue: Balancing the convenience of offering various options with the potential decrease in revenue due to higher transaction fees requires careful consideration.

Fraudulent Transactions

- Increased Risk: With more payment methods, the potential attack surface for fraudsters also increases.

- Monitoring Complexity: Monitoring transactions for fraudulent activity becomes more complex with diverse payment methods, requiring robust fraud detection and prevention systems.

- Dispute Resolution: Dealing with disputes arising from fraudulent transactions can be time-consuming and resource-intensive, requiring clear policies and procedures in place.

Mitigating these challenges

There are a number of mechanisms that can help manage the implementation of B2B payment methods on your marketplace. Here a six of the most effective ones:

- Prioritisation: Start with integrating the most popular and relevant payment methods for your target market, gradually expanding based on user demand and feedback.

- Standardisation: Explore using standardised APIs to simplify the integration process with different payment gateways.

- Security Audits: Regularly conduct security audits and penetration testing to identify and address potential vulnerabilities.

- Fee Transparency: Clearly display transaction fees associated with each payment method at the checkout stage and in relevant sections of the platform.

- Fraud Prevention: Implement robust fraud detection and prevention systems, including tools for transaction monitoring and risk analysis.

- Dispute Resolution Policy: Establish a clear dispute resolution policy outlining procedures for handling fraudulent activity claims.

Common Payment Options in B2B Online Marketplaces

Common payment options in B2B online marketplaces include credit cards, ACH payments, wire transfers, digital payment platforms, paper checks, and cash. Each option has its own advantages and disadvantages, and the choice depends on factors such as transaction size, frequency, and the parties involved. Let’s take a closer look at a few:

- PayPal: A popular choice, but what happens if a seller doesn’t have a PayPal account? PayPal’s Marketplace solution can come to the rescue, allowing buyers to pay via PayPal while sellers receive funds through other means.

- American Express: While widely accepted, some businesses might shy away from this option due to higher fees.

- Subscription Payments: Some B2B marketplaces, like Salesforce AppExchange, use a subscription model, providing steady revenue and simplifying the payment process for buyers.

- Buy Now, Pay Later Services: Services like Klarna offer flexibility, especially to smaller businesses, and can be integrated with Stripe Connect, making them an attractive option for many businesses.

Compliance Requirements in B2B Transactions

Regulatory requirements can affect your choice of payment options. For one, payments between buyers and sellers cannot pass through the accounts of unlicensed platforms.

B2B marketplaces also often deal with high-value transactions and need to ensure they are not facilitating fraud or illegal activity. Compliance might involve verifying seller legitimacy through business licence checks, tax ID confirmation, and KYC procedures to understand the customer they are dealing with. This helps mitigate risks associated with money laundering or financing of illegal activities.

Online marketplace can ease regulatory compliance by partnering with licensed payment services providers like Stripe, which has built-in seller verification features. Check out our blog post Build Trust in Your Online Marketplace with Anti-Fraud and Compliance Mechanisms for more details on how to protect your marketplace against fraud and regulatory pitfalls.

Marketplaces may also need to apply internal compliance procedures for business reasons. B2B buyers often expect net terms, where they have a set period (e.g., 30 days) to pay after receiving goods or services. The marketplace would therefore need compliance procedures to assess creditworthiness of buyers and manage potential risks associated with outstanding payments. This could involve implementing escrow services to hold funds until certain conditions are met or integrating with credit risk assessment tools.

Payment Flow in a B2B Online Marketplace

Finally, let’s talk about payment flow. Unlike B2C, B2B purchases often involve internal approvals and procurement processes. Your marketplace should cater to this by:

Integrating with existing procurement systems: This allows seamless transfer of purchase orders and approvals within buyer organisations. It makes sense to use a payments platform like Stripe that integrates with a wide range of CRMs like Salesforce and procurement tools like Coupa.

Facilitating milestone payments: For service marketplaces, allow payments tied to project completion phases, like Upwork, which facilitates secure payouts based on milestones. Nestify‘s cleaner management app allows property managers to review work and approve shifts, which triggers payouts to cleaners.